Draw on September 1, 2026

Buying a used car is a smart financial decision to avoid the massive depreciation of the first few years. However, the price on the windshield is only the tip of the iceberg.

To make an informed choice, you need to understand two things: how your financing works and what expenses will be added to your monthly payments. Here is our guide to leaving nothing to chance.

Financing is often perceived as complex, but it is based on three pillars:

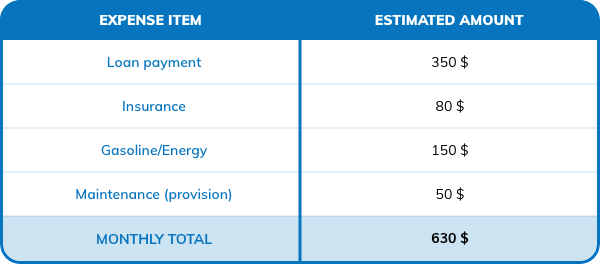

A common mistake is budgeting only for the car loan. To get a clear picture, you must include “invisible” costs:

Auto insurance

A newer vehicle or a sport model can increase your premiums. Tip: Get an insurance quote before signing the purchase contract to avoid surprises.

Preventive maintenance

Even if the vehicle is inspected, set aside an annual amount for normal maintenance: oil changes, brakes, winter tires, and rust protection treatment.

Taxes and registration

In Quebec, remember that sales tax applies. Depending on the model (for example, high-displacement engines), annual registration fees may also vary.

A rule of thumb often suggested by financial experts is the 15% rule: your total transportation costs (loan + insurance + fuel) should ideally not exceed 15% of your net monthly income.

This is the question that comes up most often, and the short answer is: Yes, but much less than you think, and not in the way you imagine.

Here is the crucial distinction to understand:

2. Credit shopping: The good news

The algorithms of Equifax and TransUnion are not naive. They know that if you are shopping for a car, you may visit two or three dealerships.

3. Why it’s better to let a professional check

Some buyers try to hide their file or give vague information out of fear of an “investigation”. This is often a mistake.

By letting your finance manager submit an official application, they can present your file in the best possible way to lenders. A temporary drop of 5 points on your credit is a small price to pay for an interest rate that could save you $2,000 over the life of your loan.

The best way to shop stress-free is to obtain credit pre-approval through your dealership. This allows you to know your rate and maximum budget before you even fall in love with a vehicle.

Need help with your calculations? Our financing specialists are here to simplify the process with you, without pressure and in complete transparency.